Adverse Media Screening Requirements Around the World

The global news landscape evolves quickly and breaking stories often indicate that customers, clients, and other parties pose a threat to an organization’s reputation or compliance liability before that information is confirmed by official sources. With that in mind, adverse media screening, also known as negative news screening, is a powerful compliance asset, helping firms anticipate and identify risks, and make decisions about effective compliance responses.

Adverse media screening is valuable at every stage of a business relationship and a cornerstone of the customer due diligence (CDD) and enhanced due diligence (EDD) processes. Organizations should seek to screen for adverse media during onboarding to help accurately establish a customer’s risk profile, and then – if warranted – throughout the relationship as a way to detect changes in risk, or to provide supplementary data for related compliance processes.

The compliance value of adverse media is reflected in the focus of regulators around the world, many of which impose adverse media screening requirements on organizations that operate within their jurisdiction. However, adverse media regulation is a challenging administrative proposition and often applied with less structure than other compliance requirements – such as PEP screening, sanctions and watchlist screening, and transaction monitoring.

Given the regulatory uncertainty, organizations must think carefully about how they implement their adverse media solutions as part of their broader regulatory compliance commitments and understand whether their solutions are compatible with the expectations of jurisdictional authorities.

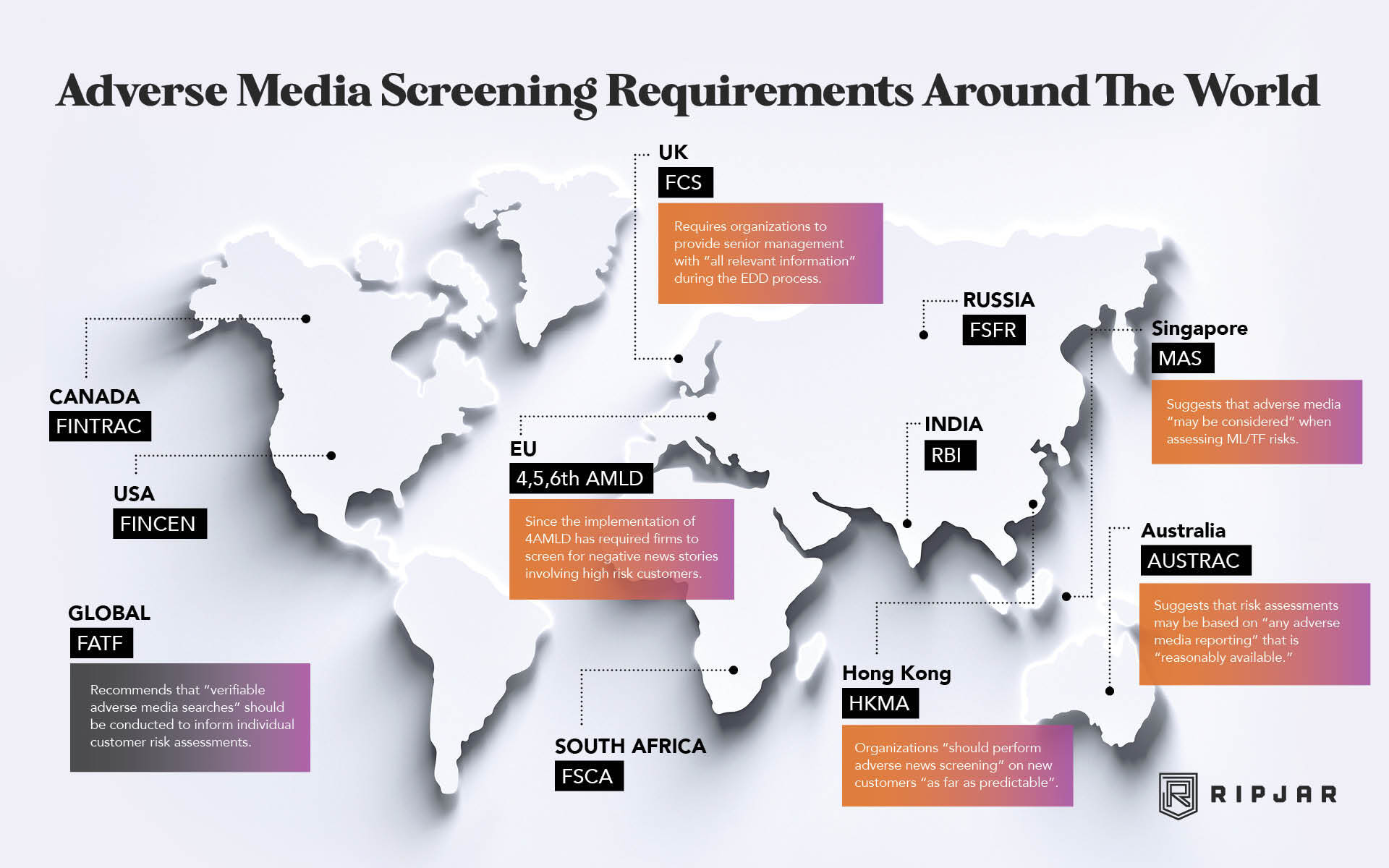

Adverse media screening features in financial compliance regulation in jurisdictions around the world. Who are the regulators that have set out adverse media recommendations and regulations – and how strictly are they applied?

Explore our illustrative map to learn more about the legal requirements and recommendations for adverse media screening in different countries around the world.

Global Adverse Media: FATF

The Financial Action Task Force (FATF) includes adverse media screening in its anti-money laundering guidance, as part of its recommendation that organizations implement a risk-based approach to compliance. Practically, the risk-based approach requires organizations to deploy a proportionate compliance response based on an assessment of the risk that individual customers and clients present. Accordingly, low risk customers may be subject to simplified AML/CFT customer due diligence measures, while higher risk customers should be subjected to enhanced due diligence which should include adverse media screening.

FATF adverse media screening guidelines suggest that organizations deploy “verifiable adverse media searches” in order to build out their client’s risk profiles and to understand the nature of the business in which they are engaged. The adverse media searches should involve the gathering of “sufficient… publicly available information” during the CDD and EDD processes.

FATF also requires organizations to establish whether customers have been subject to historic criminal investigations or regulatory penalties – which may involve historic adverse media screening. Historic actions against customers should inform their current risk categorization.

European Adverse Media: 6AMLD

The EU Parliament has mandated adverse media screening measures as part of its periodically-released Anti-Money Laundering Directives (AMLD) which member states must transpose into domestic law. The most recent of these directives is the sixth – usually known as 6AMLD – but previous directives also set out adverse media compliance requirements.

The Fourth Anti-Money Laundering Directive (4AMLD), which came into effect on 26 June 2017, included a requirement for screening against “open source” media, such as “reports in reputable newspapers”, as part of the EDD process. On 10 January 2020, 5AMLD came into effect and strengthened adverse media requirements by expanding the number of business sectors that were required to perform searches. 5AMLD also intensified the regulatory push towards compliance automation, including the use of automated adverse media screening technology.

The Sixth Anti-Money Laundering Directive came into effect on 3 June 2021. Amongst 6AMLD’s regulatory changes was a codification of 22 money laundering predicate offences – with the addition of cybercrime and environmental crime to the list. Accordingly, under 6AMLD, adverse media screening solutions must be adjusted to account for the new predicate offences as risk liabilities.

UK Adverse Media: FCA

The UK’s Financial Conduct Authority, reflects the guidance of the FATF, stipulating that adverse media screening should be implemented when onboarding customers and during “periodic reviews” of customer relationships.

The FCA referenced the importance of adverse media screening in the UK in a letter sent to retail banks in May 2021. The letter detailed a range of transaction monitoring failures by UK banks, and emphasized a particular case in which a bank had failed to act on adverse media stories that revealed allegations about illegally-obtained funds. The FCA stated that the failure had put the bank “at significant risk of facilitating money laundering”.

APAC Adverse Media: MAS, HKMA, AUSTRAC

Adverse media screening is a feature of regulatory regimes across APAC. Following FATF guidance, the Monetary Authority of Singapore (MAS) requires organizations to put suitable screening measures in place when establishing business relationships, including “screening against ML/TF information sources” such as media outlets. In 2020, MAS released a guidance paper on ‘Effective AML/CFT Controls in Private Banking’, setting out the need for organizations to monitor “adverse news” as part of their approach to risk management.

Like MAS, the Hong Kong Monetary Authority (HKMA) has underlined the importance of adverse media screening as a way to inform customer risk profiles in financial contexts. In a January 2021 publication, MAS identified adverse media searches as “ideal candidates” for automation in a regtech-integrated AML solution, and recommended the use of news media databases to facilitate those searches.

Adverse media screening features prominently in AML/CFT compliance guidance from the Australian Transaction Reports and Analysis Centre (AUSTRAC). In order to build accurate and effective customer risk profiles, AUSTRAC recommends adverse media screening as part of the CDD process during onboarding and then throughout a customer relationship in order to detect material changes in risk.